Originally appeared on The Morning

By Dhananath Fernando

Last Monday (3), Finance Minister Basil Rajapaksa announced a relief package worth Rs. 229 billion. This package consists of a Rs. 5,000 allowance for government workers, 500 g wheat flour for estate communities per day, an increase in the purchasing price of paddy by Rs. 25 to Rs. 75 a kilogramme to assist farmers, a Rs. 1,000 increase for Samurdhi beneficiaries and an incentive scheme for home gardening. When evaluating relief packages, a long list of factors should be considered. One such factor is inflation. It is no secret that there is creeping inflation affecting the livelihoods of all cross sections of society. This is openly being expressed to politicians. Food inflation is at 22% and headline inflation is at 12%.

This column has always highlighted the grave dangers of high inflation. We have been closely following these developments and our prediction has now been admitted by the Government. The sources for financing the Rs. 229 billion was not specified. The Finance Minister only mentioned that it would be utilised from the 2022 Budget while also mentioning that no tax will be increased. Both the budget numbers and their justification in the text were problematic. Inflation is the worst tax which hurts the poor more than middle income families.

Given these circumstances, the available options are to cut down some of the already allocated capital expenditure or to borrow money from the Central Bank to finance this new expense. The former is happening already, as when the Government made reductions in capital expenditure as per the budget speech. Some were manifested through policy decisions such as halting construction activities for the next two years. Therefore, if there is a reduction in capital expenditure, it will have to come through cutting down budget lines allocated to areas such as highways, road development, education, and health care.

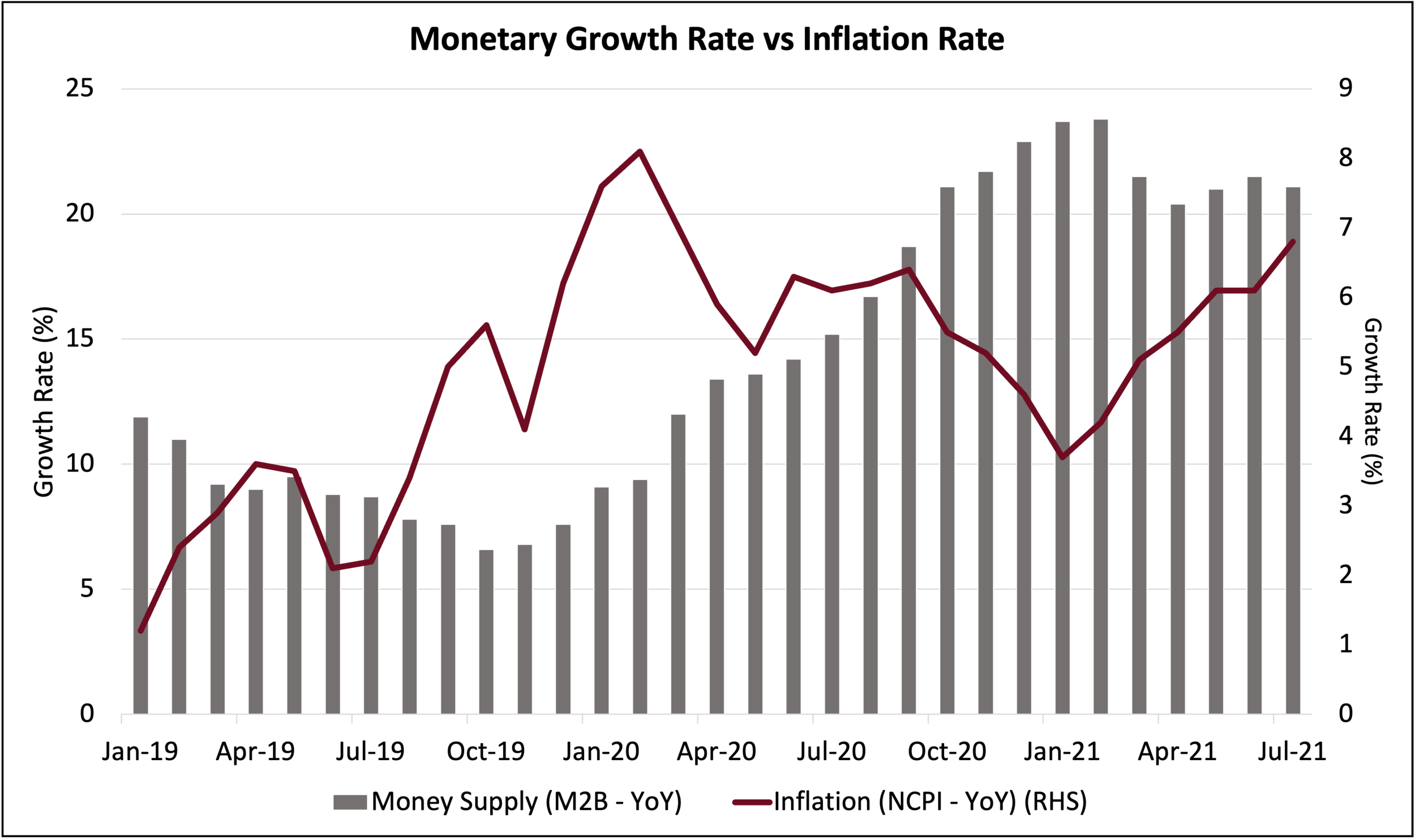

Alternatively, we may have to finance this by borrowing more money from the Central Bank, continuing the dangerous policy of believing in Modern Monetary Theory. It will have a very high risk of starting a wage spiral and contributing further to inflation and the depreciation of our currency faster than we expect. Most of this (extra) money will be spent on imported goods. This increase of demand on imports will continue to dry up our limited foriegn reserves.

In my view, the announcement will confuse investors and businesses, putting the credibility of the Finance Minister at risk. Presenting the Appropriation Bill, the Finance Minister used an anecdote to express how our economy is trapped between three competing challenges. The proposals of the budget such as to cut down expenditure by cutting down the fuel quota and extending the pension entitlement for 10 years for parliamentarians, was a positive signal. However, announcing a relief package completely opposing this may cause further business uncertainty.

An ideal relief package

While a relief package has its own pros and cons in politics and economics, it is worthwhile to explore how the relief package should be structured. As this column expressed multiple times, the only solution to overcome this crisis is through structural reforms. Structural reforms will be initially painful across the board, specially for low income earners. Pressure is already upon them with high inflation, and this demographic is being forced to make sacrifices to their food basket.

The long-term solution for this problem is establishing a digital cash transfer system based on market prices. For example, a fisherman may consume a fair share of fuel to generate income and to contribute to the economy. But the consumption of fuel of a daily wage earning labourer is limited. So the fuel subsidy has to be targeted more towards the fisherman and less towards the labourer. A digital cash transfer to the bank account based on market prices of fuel is the most efficient way of undertaking this. If we try to keep the entire fuel price low through a non-targeted system, consumers who consume more and can afford market prices will automatically benefit as well. At the same time it may be an incentive for low fuel economic machines to be used when fuel prices are low across the board. A cash transfer will not only provide dignity for a person to consume based on their needs, but also provides freedom of choice to shift to alternatives.

Making it a cash transfer avoids political interference where beneficiaries need not worry about their political opinion in order to be entitled for the scheme. Governments can also save resources and be more efficient by adhering to the market forces of demand and supply.

The Samurdhi programme which is the main safety net in Sri Lanka is very poorly targeted and about half our households have become entitled to it. Additionally, about 25% of the Samurdhi fund is spent on administration costs. Therefore, a direct cash transfer can be more efficient than Samurdhi by saving administration costs.

India administers a system called Adhar with a colour-coded system, where the value of the cash transfer is determined based on the level of poverty. In addition to being based on the poverty level, the option of managing the cash transfer in subsidies often varies with global prices of fuel and liquid petroleum gas.

Unfortunately, the relief package which was announced did not have the depth necessary, and the targeting could have been better. If we look at the public service, it is usually overstaffed and worker category cardres who are entitled for overtime are maintained by the Sri Lankan Government. As a result, in addition to the basic pay, people simply sign up for overtime work without really having the need to commit for overtime. On multiple occasions many board chairpersons and senior officers have mentioned that they sign off on overtime for their staff assistants and chauffeurs, where in most cases, the total take-home pay is higher than that of the chairman or the senior officer. As such, providing a Rs. 5,000 allowance with non-existing resources would not really help to overcome the crisis.

Sri Lanka should move towards a digital cash transfer system to strengthen our safety net. But simply strengthening the safety net won’t help the poor. Making imports competitive, bringing down tariffs on essentials and connecting with global value chains is of paramount importance in order to help the poor out of poverty.

The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute or anyone affiliated with the institute.