Originally appeared on The Morning

By Dhananath Fernando

How we end up footing the bill for Government price controls

Purchasing alcohol was an expensive endeavour back in college. I remember the total alcohol bill being shared equally amongst those who drink and those who don’t. Sri Lanka’s fuel pricing mechanism is quite similar to this. The subsidised prices are a blessing for direct users of fuel who can afford it. The majority, who are secondary users, end up paying for the subsidy indirectly. Sri Lanka’s fuel problem is quite complex. If we are to overcome this issue it is vital that policymakers understand the concept of “markets” and “prices”.

It is important that Sri Lanka integrates with global markets and continues to allow fuel imports. This costs the Government approximately about $ 3.5 billion per annum. Global fuel prices fluctuate based on market conditions, and it is crucial to understand why prices fluctuate and the indicators of these fluctuations. Some oil deposits in the world are located such that their extraction process is relatively easy and less costly. Some others are very costly to extract. The Middle East and the OPEC (Organisation of the Petroleum Exporting Countries) are reputed for their oil reserves, whereas the extraction of oil is comparatively more costly in areas like Alberta, Canada. Global oil prices are determined based on this ability of countries to supply to the global market. Political, economic, and climatic developments, and changes in these countries have a direct impact on global oil prices.

So what does the “price” increase communicate? It communicates to the consumer the scarcity of that particular resource within the particular time frame. So increases in global oil “prices” is an indication to consumers that fuel is becoming a scarce resource, and we have to use it optimally. It is also an indication to producers that they can earn more by producing more. This narrows down to the basics of supply and demand. Price is an indicator of scarcity. The “market economy” is not complicated, it is merely allowing the “price system” to work. This allows prices to indicate what should be done. Price is not just a number or a sum a consumer pays. Final retail prices are an accumulation of labour costs, material costs, scarcity, externalities, and factors of production. This is fundamentally why we must not intervene in the market price mechanism.

Sri Lanka has always ignored market principles. The island nation has been trying to artificially keep fuel prices constant despite the continuous fluctuations of global prices. We have failed to understand that such fabricated interventions to either inflate or deflate prices will only result in ceasing to keep up with global indications on whether the resource is scarce or not.

Sri Lanka’s fiscal discipline and stability has always been connected to fuel and the Ceylon Petroleum Corporation (CPC). As a result of fuel price changes, there are significant knock-on effects on all utilities, including electricity and water. CPC provides fuel at a lower price to the Ceylon Electricity Board (CEB), which is one of the main sources for electricity generation. As a result, the pricing of electricity is also now not indicative of scarcity. The CPC, which buys fuel at higher prices and sells it lower, now owes significant debts to most of the state banks.

The debt incurred is in US dollar terms. A delay in payment or a default may adversely affect the entire financial system. The heavy impact this would have on the banking sector will consequently impact the Central Bank of Sri Lanka (CBSL). It is no secret that the CBSL bails out the CPC and CEB through Treasury Bills, or by printing money. Therefore it is clear that by intervening, we have successfully exposed the entire financial system to deep peril.

The current Minister of Energy said the banks have informed the CPC Chairman that they do not have foreign currency to pay for fuel imports. This was informed to the Secretary of the Treasury, who then summoned all the heads of banks, who collectively assured the payments for fuel imports. He further stated that the CBSL said it cannot offer any reserves, given the country’s economic woes. It is perplexing to say that the problem is really this severe. It is clear that intervention in the price system has caused a massive domino effect beyond comprehension.

According to a World Bank report, the biggest beneficiary of subsidised fuel prices are the highest echelons of society. “The non-poor are the largest consumers of fuel and electricity (the top 30% of society consumes 70% of fuel. This is well ahead of direct and indirect consumption of fuel by the bottom 40% through public transport). The administered fuel prices are an effective subsidy to the non-poor funded indirectly by fiscal resources,” stated the World Bank in its Development Update for Sri Lanka in November 2017.

I see no difference in this fuel pricing phenomenon and how the final alcohol bill was shared amongst those who drink and those who don’t in my college days. The poor are bearing the burden of fuel subsidies so the rich can buy fuel for much cheaper. The weighed-down poor only consume fuel in the form of transport, electricity, and other secondary forms. We have to understand that the losses of the CPC have to be paid by someone. Currently, that someone is constituted by both the rich and the poor.

One important aspect is that the Government also collects revenue through the consumption of fuel. Changes made to the duty waiver have caused enormous losses to the Government. Giving cash subsidies to the poorest section of society could have been a much better strategy than tampering with duty waivers and underpricing fuel, ignoring market signals.

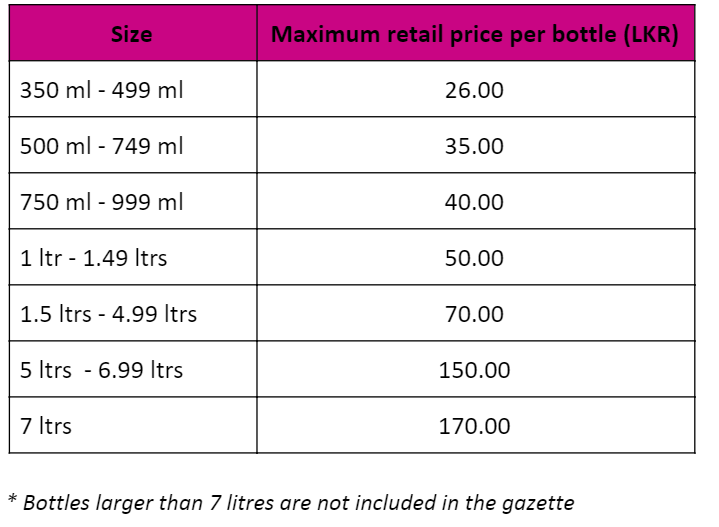

According to the calculations shown in Figure 1, the recent price changes do not reflect market prices of diesel, as illustrated in Figure 2.

What is the solution?

The first solution lies in addressing the problem. As of now, Sri Lanka’s fuel prices fail to indicate scarcity, hampering the independent function of market prices. One way of doing this is by setting up a transparent mechanism and changing the prices to reflect market prices. It may be a price formula or a process where transparency is assured.

Such a step will incentivise better resource allocation. Consumers will be able to shift between alternative choices and manage their decisions based on price signals. The previous administration introduced a pricing formula that was very poorly administered. The method of calculation was not properly communicated.

I recall a time when elections were approaching, with a simultaneous spike in global oil prices underway. However, Sri Lanka’s oil prices remained the same. The same was seen when global prices reduced during the first lockdown, and the local consumer was deprived of the deflation.

One common misperception on this strategy was voiced politically as: “Why do we need a Government if the prices are going to change according to the world market prices?” Simply because we are now experiencing the consequences of such control by the Government. As The Morning reported, the fuel fund has a negative Rs. 26 billion and there are many discrepancies over the numbers in numerous reports.

Another common misperception is that based on the price changes of fuel, we are going to allow bus fares and other connected prices to change daily. It may be daily changes or it can be changes over a month or a quarter, and there are so many ways we can structure it based on market forces. We have all forgotten that we deal with so many daily price fluctuations. Vegetable prices, Gold prices, stock market prices, and even the prices we pay as interest for Treasury Bills and Bonds change everyday. Price changes for a reason: they communicate the market conditions, which is the ultimate objective of “price”, and allowing the markets to work.

It is true that this price hike has an impact on the poor. The Government can consider direct cash transfers. The cost of cash transfers will be lower than the losses we collectively incur from the CPC, CEB, and other fuel-dependent state institutions. The current price hike is just another temporary solution; it does not fix the problem.

Increasing the share collected by everyone at my university party does not change the unfair division of the cost. Likewise, a price increase without setting up a market system and price signals to operate won’t solve Sri Lanka’s fuel and economic crisis.Purchasing alcohol was an expensive endeavour back in college. I remember the total alcohol bill being shared equally amongst those who drink and those who don’t. Sri Lanka’s fuel pricing mechanism is quite similar to this. The subsidised prices are a blessing for direct users of fuel who can afford it. The majority, who are secondary users, end up paying for the subsidy indirectly. Sri Lanka’s fuel problem is quite complex. If we are to overcome this issue it is vital that policymakers understand the concept of “markets” and “prices”.

It is important that Sri Lanka integrates with global markets and continues to allow fuel imports. This costs the Government approximately about $ 3.5 billion per annum. Global fuel prices fluctuate based on market conditions, and it is crucial to understand why prices fluctuate and the indicators of these fluctuations. Some oil deposits in the world are located such that their extraction process is relatively easy and less costly. Some others are very costly to extract. The Middle East and the OPEC (Organisation of the Petroleum Exporting Countries) are reputed for their oil reserves, whereas the extraction of oil is comparatively more costly in areas like Alberta, Canada. Global oil prices are determined based on this ability of countries to supply to the global market. Political, economic, and climatic developments, and changes in these countries have a direct impact on global oil prices.

So what does the “price” increase communicate? It communicates to the consumer the scarcity of that particular resource within the particular time frame. So increases in global oil “prices” is an indication to consumers that fuel is becoming a scarce resource, and we have to use it optimally. It is also an indication to producers that they can earn more by producing more. This narrows down to the basics of supply and demand. Price is an indicator of scarcity. The “market economy” is not complicated, it is merely allowing the “price system” to work. This allows prices to indicate what should be done. Price is not just a number or a sum a consumer pays. Final retail prices are an accumulation of labour costs, material costs, scarcity, externalities, and factors of production. This is fundamentally why we must not intervene in the market price mechanism.

Sri Lanka has always ignored market principles. The island nation has been trying to artificially keep fuel prices constant despite the continuous fluctuations of global prices. We have failed to understand that such fabricated interventions to either inflate or deflate prices will only result in ceasing to keep up with global indications on whether the resource is scarce or not.

Sri Lanka’s fiscal discipline and stability has always been connected to fuel and the Ceylon Petroleum Corporation (CPC). As a result of fuel price changes, there are significant knock-on effects on all utilities, including electricity and water. CPC provides fuel at a lower price to the Ceylon Electricity Board (CEB), which is one of the main sources for electricity generation. As a result, the pricing of electricity is also now not indicative of scarcity. The CPC, which buys fuel at higher prices and sells it lower, now owes significant debts to most of the state banks.

The debt incurred is in US dollar terms. A delay in payment or a default may adversely affect the entire financial system. The heavy impact this would have on the banking sector will consequently impact the Central Bank of Sri Lanka (CBSL). It is no secret that the CBSL bails out the CPC and CEB through Treasury Bills, or by printing money. Therefore it is clear that by intervening, we have successfully exposed the entire financial system to deep peril.

The current Minister of Energy said the banks have informed the CPC Chairman that they do not have foreign currency to pay for fuel imports. This was informed to the Secretary of the Treasury, who then summoned all the heads of banks, who collectively assured the payments for fuel imports. He further stated that the CBSL said it cannot offer any reserves, given the country’s economic woes. It is perplexing to say that the problem is really this severe. It is clear that intervention in the price system has caused a massive domino effect beyond comprehension.

According to a World Bank report, the biggest beneficiary of subsidised fuel prices are the highest echelons of society. “The non-poor are the largest consumers of fuel and electricity (the top 30% of society consumes 70% of fuel. This is well ahead of direct and indirect consumption of fuel by the bottom 40% through public transport). The administered fuel prices are an effective subsidy to the non-poor funded indirectly by fiscal resources,” stated the World Bank in its Development Update for Sri Lanka in November 2017.

I see no difference in this fuel pricing phenomenon and how the final alcohol bill was shared amongst those who drink and those who don’t in my college days. The poor are bearing the burden of fuel subsidies so the rich can buy fuel for much cheaper. The weighed-down poor only consume fuel in the form of transport, electricity, and other secondary forms. We have to understand that the losses of the CPC have to be paid by someone. Currently, that someone is constituted by both the rich and the poor.

One important aspect is that the Government also collects revenue through the consumption of fuel. Changes made to the duty waiver have caused enormous losses to the Government. Giving cash subsidies to the poorest section of society could have been a much better strategy than tampering with duty waivers and underpricing fuel, ignoring market signals.

According to the calculations shown in Figure 1, the recent price changes do not reflect market prices of diesel, as illustrated in Figure 2.

What is the solution?

The first solution lies in addressing the problem. As of now, Sri Lanka’s fuel prices fail to indicate scarcity, hampering the independent function of market prices. One way of doing this is by setting up a transparent mechanism and changing the prices to reflect market prices. It may be a price formula or a process where transparency is assured.

Such a step will incentivise better resource allocation. Consumers will be able to shift between alternative choices and manage their decisions based on price signals. The previous administration introduced a pricing formula that was very poorly administered. The method of calculation was not properly communicated.

I recall a time when elections were approaching, with a simultaneous spike in global oil prices underway. However, Sri Lanka’s oil prices remained the same. The same was seen when global prices reduced during the first lockdown, and the local consumer was deprived of the deflation.

One common misperception on this strategy was voiced politically as: “Why do we need a Government if the prices are going to change according to the world market prices?” Simply because we are now experiencing the consequences of such control by the Government. As The Morning reported, the fuel fund has a negative Rs. 26 billion and there are many discrepancies over the numbers in numerous reports.

Another common misperception is that based on the price changes of fuel, we are going to allow bus fares and other connected prices to change daily. It may be daily changes or it can be changes over a month or a quarter, and there are so many ways we can structure it based on market forces. We have all forgotten that we deal with so many daily price fluctuations. Vegetable prices, Gold prices, stock market prices, and even the prices we pay as interest for Treasury Bills and Bonds change everyday. Price changes for a reason: they communicate the market conditions, which is the ultimate objective of “price”, and allowing the markets to work.

It is true that this price hike has an impact on the poor. The Government can consider direct cash transfers. The cost of cash transfers will be lower than the losses we collectively incur from the CPC, CEB, and other fuel-dependent state institutions. The current price hike is just another temporary solution; it does not fix the problem.

Increasing the share collected by everyone at my university party does not change the unfair division of the cost. Likewise, a price increase without setting up a market system and price signals to operate won’t solve Sri Lanka’s fuel and economic crisis.Purchasing alcohol was an expensive endeavour back in college. I remember the total alcohol bill being shared equally amongst those who drink and those who don’t. Sri Lanka’s fuel pricing mechanism is quite similar to this. The subsidised prices are a blessing for direct users of fuel who can afford it. The majority, who are secondary users, end up paying for the subsidy indirectly. Sri Lanka’s fuel problem is quite complex. If we are to overcome this issue it is vital that policymakers understand the concept of “markets” and “prices”.

It is important that Sri Lanka integrates with global markets and continues to allow fuel imports. This costs the Government approximately about $ 3.5 billion per annum. Global fuel prices fluctuate based on market conditions, and it is crucial to understand why prices fluctuate and the indicators of these fluctuations. Some oil deposits in the world are located such that their extraction process is relatively easy and less costly. Some others are very costly to extract. The Middle East and the OPEC (Organisation of the Petroleum Exporting Countries) are reputed for their oil reserves, whereas the extraction of oil is comparatively more costly in areas like Alberta, Canada. Global oil prices are determined based on this ability of countries to supply to the global market. Political, economic, and climatic developments, and changes in these countries have a direct impact on global oil prices.

So what does the “price” increase communicate? It communicates to the consumer the scarcity of that particular resource within the particular time frame. So increases in global oil “prices” is an indication to consumers that fuel is becoming a scarce resource, and we have to use it optimally. It is also an indication to producers that they can earn more by producing more. This narrows down to the basics of supply and demand. Price is an indicator of scarcity. The “market economy” is not complicated, it is merely allowing the “price system” to work. This allows prices to indicate what should be done. Price is not just a number or a sum a consumer pays. Final retail prices are an accumulation of labour costs, material costs, scarcity, externalities, and factors of production. This is fundamentally why we must not intervene in the market price mechanism.

Sri Lanka has always ignored market principles. The island nation has been trying to artificially keep fuel prices constant despite the continuous fluctuations of global prices. We have failed to understand that such fabricated interventions to either inflate or deflate prices will only result in ceasing to keep up with global indications on whether the resource is scarce or not.

Sri Lanka’s fiscal discipline and stability has always been connected to fuel and the Ceylon Petroleum Corporation (CPC). As a result of fuel price changes, there are significant knock-on effects on all utilities, including electricity and water. CPC provides fuel at a lower price to the Ceylon Electricity Board (CEB), which is one of the main sources for electricity generation. As a result, the pricing of electricity is also now not indicative of scarcity. The CPC, which buys fuel at higher prices and sells it lower, now owes significant debts to most of the state banks.

The debt incurred is in US dollar terms. A delay in payment or a default may adversely affect the entire financial system. The heavy impact this would have on the banking sector will consequently impact the Central Bank of Sri Lanka (CBSL). It is no secret that the CBSL bails out the CPC and CEB through Treasury Bills, or by printing money. Therefore it is clear that by intervening, we have successfully exposed the entire financial system to deep peril.

The current Minister of Energy said the banks have informed the CPC Chairman that they do not have foreign currency to pay for fuel imports. This was informed to the Secretary of the Treasury, who then summoned all the heads of banks, who collectively assured the payments for fuel imports. He further stated that the CBSL said it cannot offer any reserves, given the country’s economic woes. It is perplexing to say that the problem is really this severe. It is clear that intervention in the price system has caused a massive domino effect beyond comprehension.

According to a World Bank report, the biggest beneficiary of subsidised fuel prices are the highest echelons of society. “The non-poor are the largest consumers of fuel and electricity (the top 30% of society consumes 70% of fuel. This is well ahead of direct and indirect consumption of fuel by the bottom 40% through public transport). The administered fuel prices are an effective subsidy to the non-poor funded indirectly by fiscal resources,” stated the World Bank in its Development Update for Sri Lanka in November 2017.

I see no difference in this fuel pricing phenomenon and how the final alcohol bill was shared amongst those who drink and those who don’t in my college days. The poor are bearing the burden of fuel subsidies so the rich can buy fuel for much cheaper. The weighed-down poor only consume fuel in the form of transport, electricity, and other secondary forms. We have to understand that the losses of the CPC have to be paid by someone. Currently, that someone is constituted by both the rich and the poor.

One important aspect is that the Government also collects revenue through the consumption of fuel. Changes made to the duty waiver have caused enormous losses to the Government. Giving cash subsidies to the poorest section of society could have been a much better strategy than tampering with duty waivers and underpricing fuel, ignoring market signals.

According to the calculations shown in Figure 1, the recent price changes do not reflect market prices of diesel, as illustrated in Figure 2.

What is the solution?

The first solution lies in addressing the problem. As of now, Sri Lanka’s fuel prices fail to indicate scarcity, hampering the independent function of market prices. One way of doing this is by setting up a transparent mechanism and changing the prices to reflect market prices. It may be a price formula or a process where transparency is assured.

Such a step will incentivise better resource allocation. Consumers will be able to shift between alternative choices and manage their decisions based on price signals. The previous administration introduced a pricing formula that was very poorly administered. The method of calculation was not properly communicated.

I recall a time when elections were approaching, with a simultaneous spike in global oil prices underway. However, Sri Lanka’s oil prices remained the same. The same was seen when global prices reduced during the first lockdown, and the local consumer was deprived of the deflation.

One common misperception on this strategy was voiced politically as: “Why do we need a Government if the prices are going to change according to the world market prices?” Simply because we are now experiencing the consequences of such control by the Government. As The Morning reported, the fuel fund has a negative Rs. 26 billion and there are many discrepancies over the numbers in numerous reports.

Another common misperception is that based on the price changes of fuel, we are going to allow bus fares and other connected prices to change daily. It may be daily changes or it can be changes over a month or a quarter, and there are so many ways we can structure it based on market forces. We have all forgotten that we deal with so many daily price fluctuations. Vegetable prices, Gold prices, stock market prices, and even the prices we pay as interest for Treasury Bills and Bonds change everyday. Price changes for a reason: they communicate the market conditions, which is the ultimate objective of “price”, and allowing the markets to work.

It is true that this price hike has an impact on the poor. The Government can consider direct cash transfers. The cost of cash transfers will be lower than the losses we collectively incur from the CPC, CEB, and other fuel-dependent state institutions. The current price hike is just another temporary solution; it does not fix the problem.

Increasing the share collected by everyone at my university party does not change the unfair division of the cost. Likewise, a price increase without setting up a market system and price signals to operate won’t solve Sri Lanka’s fuel and economic crisis.