By Dhananath Fernando

Originally appeared on The Morning

Sri Lanka received about $ 695 million after the combined Fifth and Sixth Reviews of the International Monetary Fund (IMF) Extended Fund Facility. It is an important milestone. It gives the country some breathing space. It also confirms that we have done many things right since the crisis. But it also brings us closer to a reality check.

After almost four years of crisis management, we are beginning to realise that we have done very little beyond stabilisation. We fixed many of the things the IMF asked us to fix. We increased taxes. We restored cost reflective pricing. We improved fiscal discipline. We passed some important laws. We rebuilt some confidence.

But we have not done the big growth reforms this column has been arguing for over many years. The IMF programme has about nine months to go. The uncomfortable question is simple. What have we done to grow after the IMF programme ends?

Better numbers don’t mean a stronger economy

The answer is not very encouraging.

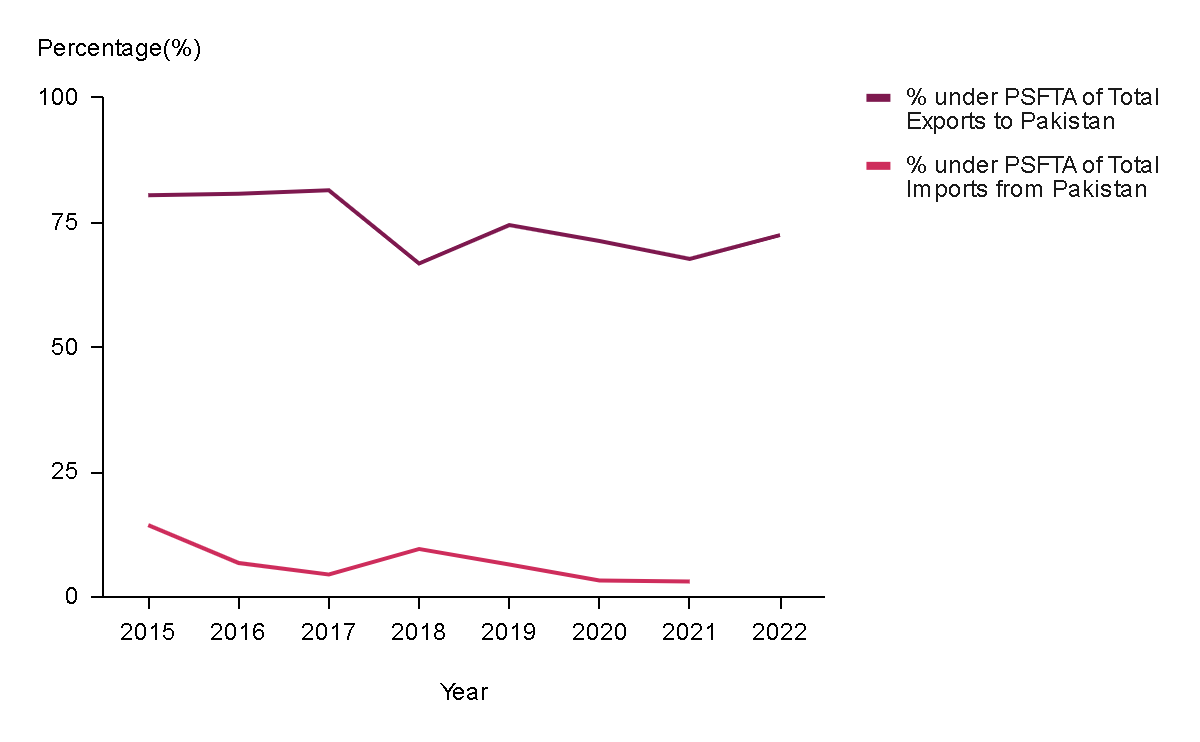

Land reforms for industries have been slow. Labour reforms that can respond to a declining labour force and very low female labour force participation have been pushed back. State-Owned Enterprise (SOE) reforms that can unlock economic resources and reduce fiscal risks have not moved at the required speed. Investment reforms, including a serious reform of the Board of Investment, are still largely under discussion. Trade agreements and better access to global markets have been kept on the backburner for political convenience.

What we have mainly done is revenue enhancement. Even there, a significant part of the recent improvement has come from vehicle imports. This is not a sustainable growth strategy.

Vehicle imports were reopened after years of restrictions. Naturally, there was pent-up demand. Imports surged. The Treasury received a large amount of revenue from duties and taxes. But this is a one-off source. We cannot import the same volume of vehicles every year and call it fiscal strength.

Already, vehicle registrations are slowing. The Government has also imposed an additional surcharge on Customs duty. That may bring some short-term revenue, but it also signals how dependent we have become on taxing imports rather than expanding the productive economy.

This is precisely the danger. We may come out of the IMF programme with better numbers, but without a stronger economy.

Some reforms have been scheduled so far into the future that they may never happen. Para-tariff removals, for instance, are expected to be phased out only by 2029; that is after the current IMF programme. The longer the delay, the more time lobbying groups have to protect their privileges. In Sri Lanka, reforms postponed are often reforms abandoned.

The post-IMF landscape

So what happens after the IMF programme?

Without growth reforms, we will slowly slide back. Not immediately. Not dramatically. But gradually. First, investment will remain weak. Then jobs will not grow fast enough. Then tax revenue will disappoint. Then debt repayment pressure will rise. Then the exchange rate will come under pressure. Then the same old arguments will return: control imports, subsidise energy, print money, blame external forces.

Unfortunately, external forces are not helping us either.

The IMF itself has warned that Sri Lanka’s 2026 growth outlook has weakened, with growth projected at around 3%. The Middle East conflict and the aftermath of Cyclone Ditwah have tilted risks to the downside. Higher oil prices can increase inflation, weaken the current account, and affect tourism. These are not theoretical risks for Sri Lanka. We are an energy-importing country. We do not have much room to absorb large shocks.

If rainfall weakens and hydropower generation drops, diesel-based power generation will rise. That means electricity costs will rise. If global diesel and crude prices rise further, the pressure will come through fuel, electricity, transport, food, and construction materials. Aluminium, steel, fertiliser, and agricultural products will also feel the impact through energy and logistics costs.

This is the problem with a weak economy. A global shock becomes a domestic crisis very quickly.

The IMF has also been clear that debt sustainability risks remain high. The debt trajectory can improve only if we maintain strong fiscal performance, keep inflation under control, and sustain growth. From 2027 onwards, Sri Lanka is expected to return to a primary balance target of 2.3% of GDP. That is not easy if growth is weak and revenue depends heavily on temporary windfalls such as vehicle imports.

In other words, the IMF programme can help us stabilise. But it cannot make us rich. It cannot create jobs for us. It cannot make our exports competitive. It cannot bring investors if our land, labour, tax, trade, and regulatory systems remain difficult. It cannot make our SOEs efficient if we do not have the political courage to reform them.

The IMF is not a substitute for a national growth strategy.

Building an economy that can stand on its own

What are the solutions?

There is no shortcut. We have to become responsible and do the growth reforms ourselves. The crisis forced us to do stabilisation reforms because the alternative was collapse. But growth reforms require a different kind of political courage. They do not always produce immediate results. They upset vested interests. They require explaining difficult choices to the public.

That is why we have avoided them.

If we cannot build that political will ourselves, we may again be pushed towards another IMF arrangement after this programme. There are IMF arrangements that may not require new money but can still provide policy credibility. Such an arrangement can reassure investors, reduce risk premiums, and lower borrowing costs. But politically, an IMF programme without money is a very difficult message to sell.

More importantly, another IMF programme can also become another way of kicking the can down the road. If growth reforms are not front-loaded, we will again reach the end of the next programme and ask the same question: what have we done for growth?

The better option is to build a domestic political consensus before the pressure returns.

Just as we have a Constitutional Council for important appointments, Sri Lanka needs a minimum national growth agenda agreed by the main political parties. It need not cover everything. It should focus on a few reforms that can deliver growth and jobs: land for investment, labour flexibility, public transport, SOE reform, faster investment approvals, trade facilitation, and a predictable tax regime.

The objective must be clear: Sri Lanka should aim for 5–8% growth, not 3% survival.

Some reforms can show results faster than others. Public transport reform can improve productivity quickly because millions of people lose time every day in bad transport. Labour reforms can help more women and young people enter the workforce. Investment approval reforms can quickly improve investor confidence. SOE reforms can release assets, reduce fiscal risks, and open space for private sector activity.

But these reforms must be owned by Sri Lanka, not outsourced to Washington.

The IMF has helped us avoid collapse. For that, the programme has been useful. But avoiding collapse is not the same as building prosperity. Stabilisation is the floor, not the ceiling.

The next nine months are important not because the IMF programme is ending, but because our excuse is ending. We can no longer say we are only managing the crisis. We now have to decide whether we are building an economy that can stand on its own.

By failing to reform, we are preparing ourselves to fail once again.