By Dhananath Fernando

Originally appeared on The Morning

Why has the Sri Lankan Rupee depreciated over the last few days? Many people want to know the reason. Many also want to predict where the exchange rate will stabilise.

In simple terms, the exchange rate is the price we pay in rupees to buy one US Dollar. It is similar to buying a cake of soap from a shop. If the price of soap increases, we say soap has become more expensive. Likewise, when the price of a US Dollar increases in rupee terms, we say the rupee has depreciated.

Like any other good, the price of the US Dollar is determined by demand and supply.

On the supply side, dollars come into the banking system through merchandise exports, service exports, tourism earnings, worker remittances, foreign direct investments, and other capital inflows.

The real trick is in understanding the demand side. Dollars are demanded for merchandise imports such as raw materials, fuel, vehicles, and medicine. Dollars are also needed for outbound tourism expenditure, foreign salaries, profit repatriation, and outward remittances. In addition to importers and individuals, the Central Bank too buys dollars from the market to build reserves.

So, when the demand for dollars exceeds the supply of dollars, the rupee depreciates. In other words, the price of the dollar goes up.

But there is one important point many people miss. Demand for dollars is created through rupees. If there is more rupee liquidity in the banking system, and if that liquidity is converted into credit, it can create more demand for imports and therefore more demand for dollars.

How USD demand is created: Story of excess credit

Everyone who goes to a bank to buy dollars either pays in cash or obtains a loan from the bank.

If banks lend from depositors’ money, it does not necessarily create excess demand. This is because someone has already saved money by reducing consumption. That saved money is then lent to someone else with interest. In that case, overall demand in the economy does not increase in the same way.

But the situation is different when the Central Bank buys dollars from the market to build reserves.

The Central Bank does not collect deposits from the public like a commercial bank. When the Central Bank buys dollars, it pays rupees into the banking system. In simple terms, it creates new rupees.

One may then ask: is it wrong for the Central Bank to buy dollars and build reserves? The simple answer is no. The Central Bank must build reserves, especially after a crisis. It has to buy dollars from the market to do so.

However, when the Central Bank buys dollars, new rupees enter the banking system. Over the last three years, the Central Bank has bought a cumulative $ 6,528 million from the market, injecting rupees into the banking system in the process.

Once this additional rupee liquidity is in the banking system, banks cannot earn much by simply keeping it idle. They have two options:

They can deposit the money back at the Central Bank and earn interest – This is linked to what we call the overnight policy rate. At present, if banks deposit excess money at the Central Bank, they earn about 7.25% interest.

They can lend this money to customers – These loans can take many forms: letters of credit for imports, credit cards, housing loans, overdraft facilities, business loans, and other forms of credit.

When banks extend loans using this additional rupee liquidity, credit in the economy expands. Part of this credit eventually moves into imports because people and businesses buy more goods, many of which are imported. This creates additional demand for dollars.

According to the Central Bank’s Annual Economic Review 2025, private credit expanded sharply. Credit growth increased from around 25%, and in value terms, credit expanded from about Rs. 790 billion in 2024 to about Rs. 2,000 billion in 2025. This means the economy created more demand for dollars through credit expansion.

When the economy is growing strongly, new rupee liquidity may not immediately create trouble because the new money is also used to produce and consume more goods and services. But when credit expands faster than dollar inflows, the economy becomes vulnerable. Usually, the pressure becomes visible after an internal or external shock.

In simple terms, while Sri Lanka had excess dollars in the market for some time, excess rupee liquidity and credit expansion continued to create demand for imports. That import demand eventually created pressure on the exchange rate.

Speculation effect

The second reason for the recent depreciation is speculation.

When the currency starts to depreciate, those who bring dollars into the market may hold back, expecting the rupee to depreciate further. Exporters, remitters, and others who have dollars may delay conversion.

At the same time, those who need dollars try to buy them as early as possible to avoid a further loss. Importers and businesses rush to cover their dollar needs.

As a result, demand increases while supply is delayed. This can push the exchange rate up quickly.

If this continues, informal markets can also get activated. When people feel they cannot access dollars easily through the formal banking system, or when they expect the rupee to depreciate further, they may start looking for dollars outside the formal market.

That creates another problem. The informal rate can move above the official rate, more dollar holders may delay bringing money into the formal system, and confidence in the exchange rate can weaken further.

Fuel price adjustments and vehicle import ban

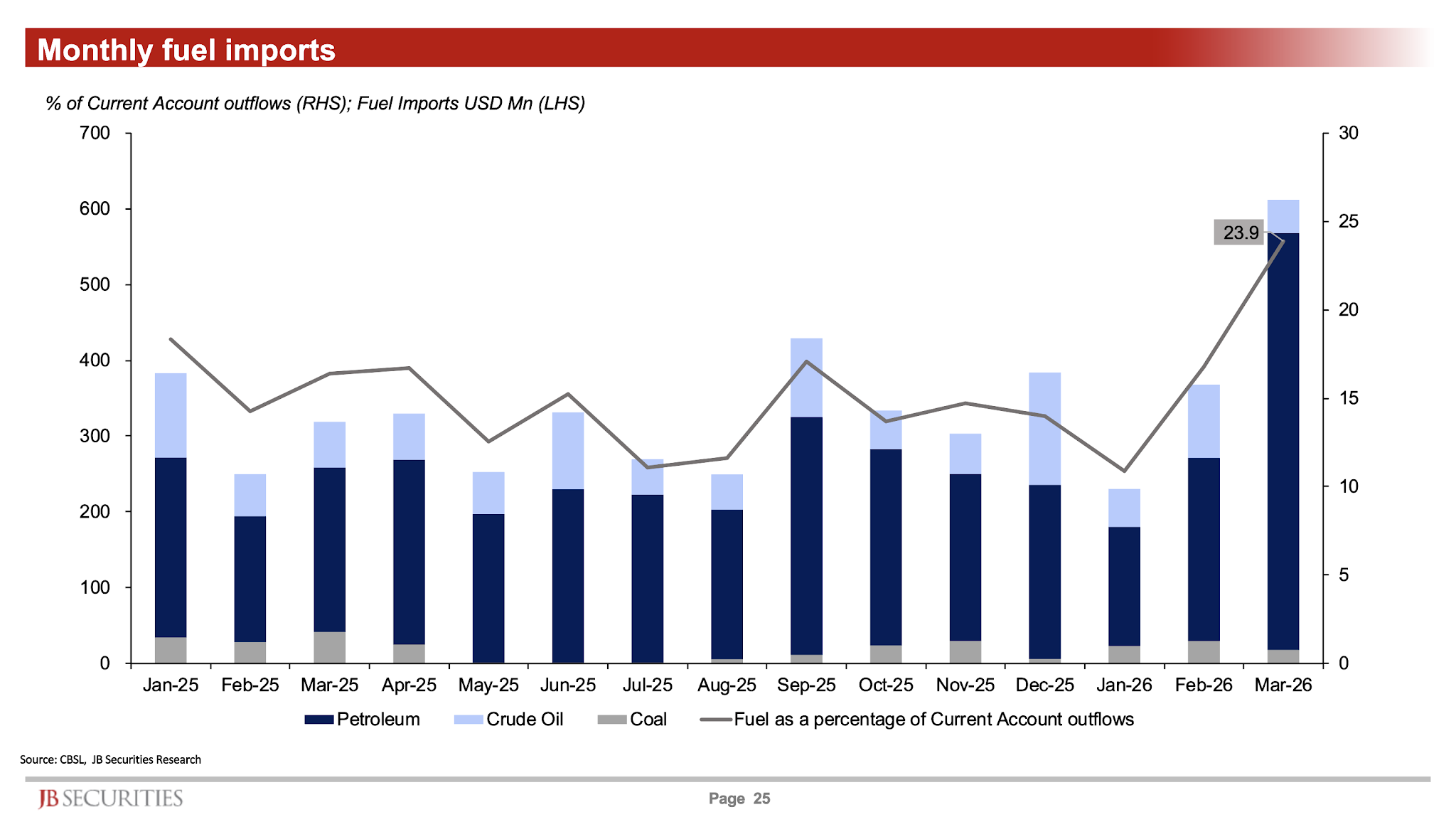

Adjusting diesel prices to market prices is essential to contain dollar demand. Fuel is one of our largest import items. In March, fuel accounted for about 23% of our imports. Therefore, fuel prices have to reflect market costs.

If fuel prices are kept artificially low, consumption does not adjust. People continue to consume fuel as if global prices have not changed. But the country still has to find dollars to pay for those imports. That is how a fuel subsidy becomes an exchange rate problem.

There is another argument that vehicle imports should be banned again to save dollars. This sounds attractive, but it does not solve the real problem.

If vehicle imports are banned while excess rupee liquidity remains in the banking system, banks will lend that money to other sectors. Credit may then move into construction, electronics, consumer goods, or other import-heavy categories. So while vehicle imports come down on one side, imports in another category can increase.

Therefore, banning one import item does not necessarily reduce overall import demand. It only shifts demand from one category to another.

If the objective is to reduce overall import demand, the real tool is interest rates. When market interest rates increase, banks have a better incentive to deposit money at the Central Bank instead of lending aggressively to customers. Higher interest rates also discourage people and businesses from taking new loans. Consumption slows down, credit slows down, and import demand comes down.

Of course, this is not painless. When interest rates go up, the economy slows. Businesses face pressure. Small and Medium-sized Enterprises (SMEs) face a difficult time. Borrowers feel the pain.

But this is the difficult choice in economic management. Either we adjust early through prices and interest rates, or we are forced to adjust later through a currency crisis.

The real reasons for exchange rate depreciation are a mix of global shocks, credit expansion, and speculation. The tools available are also clear: fuel prices must be cost-reflective, and interest rates must be used when credit expansion creates pressure on the currency.

Both actions are politically unpopular. But if we fail to adjust to reality, the reality we will face later will be far more unpopular.