Originally appeared on The Morning

By K.D.D.B Vimanga

A non-traditional budget was what the country needed. In general, budgets in Sri Lanka have mostly been giveaways to maintain political status quo or simply an outline of the Government’s plan for the economy, without taking into consideration current economic realities. As a result of numerous governments prioritising political gains over economic realities, the nation is currently experiencing severe economic consequences. These are manifested to the public in the form of steep price increases, shortages of essential goods, import restrictions, and much more. The macroeconomic consequences of this are fiscal and monetary instability, coupled with serious questions on Sri Lanka’s debt sustainability. A non-traditional budget would have indicated the broad policy direction and priorities of the Government with an understanding of where the economy is right now. The Budget would have prioritised macroeconomic stabilisation, taking into consideration the seriousness of the present economic crisis. Whether the budget proposals for 2022 achieve this remains a question.

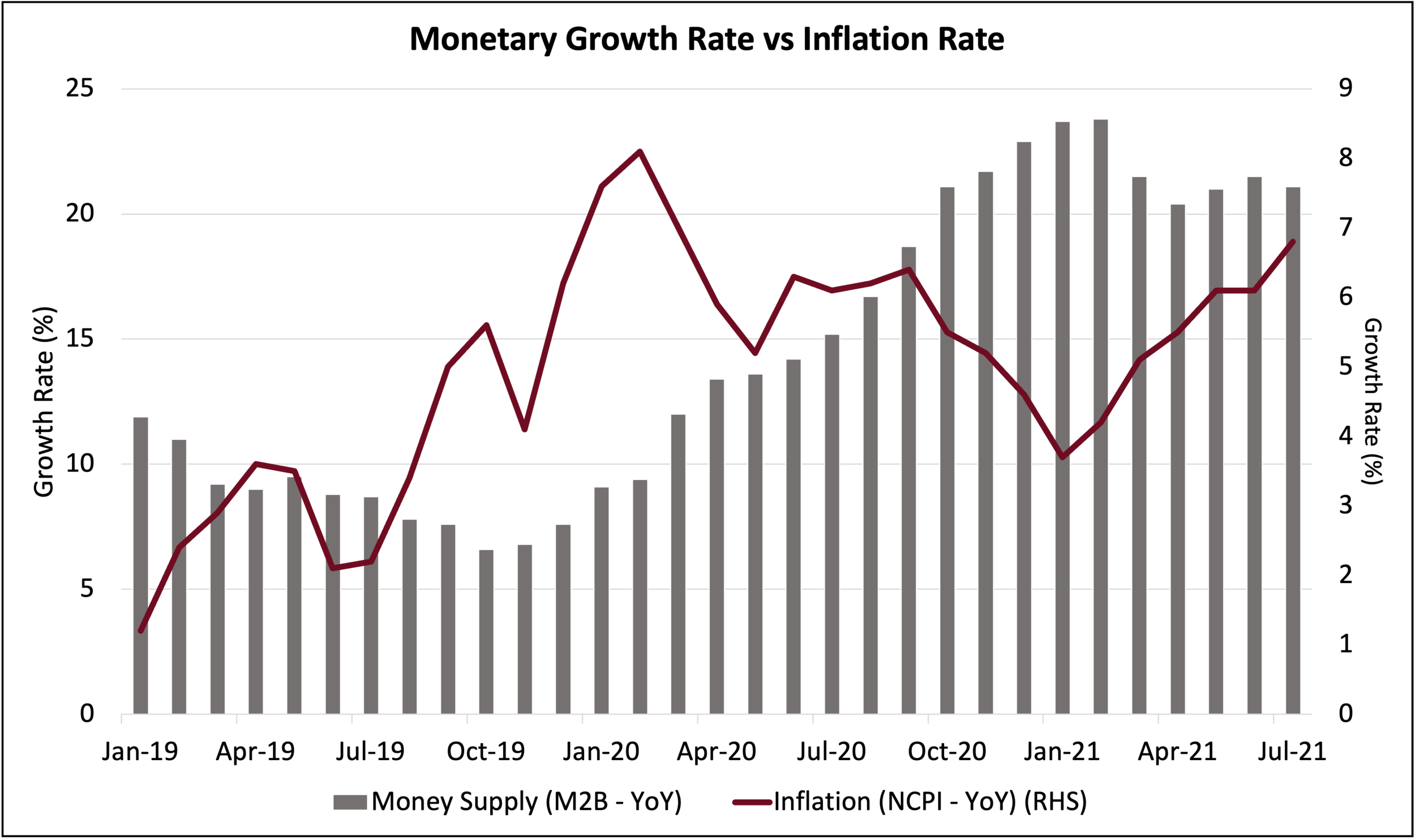

Analysing the Budget Speech makes it clear that the intention of the Budget was to be conscious of government expenditure. Is this consciousness sufficient? Especially at a time where the foreign debt service forecast for 2022 is an estimated $ 4,483.80 million? (1), when the state of the country’s foreign reserves stood at about $ 2.6 billion in September 2021 (1.7 months of imports [2]), and following which the net foreign assets have been negative in the months after. This very question of debt sustainability remains the elephant in the room. Yet, the Budget Speech failed to elaborate on specific measures that the Government hopes to utilise to meet this target. A budget that understands the present challenges would have presented a roadmap of actions to meet these outflows. The failure to do so highlights the failure to streamline the Budget to meet the seriousness of the present economic crisis.

A certain amount of credit must be given to the Government for refraining from making excessive government expenditure proposals. There is a slight increase in government total expenditure from the revised estimate of Rs. 3,387 billion for 2021 to Rs. 3,912 billion for 2022. This remains prudent in comparison to the Government’s total revenue from the revised estimate of Rs. 1,556 billion in 2021 to Rs. 2,284 billion (3). According to the figures provided by the Ministry of Finance, the budget deficit would see a reduction from Rs. 1,826 billion in 2021 to Rs. 1,628 billion in 2022. However, it should be noted that while the Budget Speech of 2021 promised a deficit of 9%, the revised estimate of the deficit has increased to 11.1% as per the Fiscal Management Report of 2022.

The budget deficit still remains unsustainably large for a country with a gross domestic product (GDP) of $ 80.7 billion in 2020 (4). The Budget tries to reduce government expenditure by proposing policies to reduce recurrent expenditure. These include reducing the fuel allowance provided to ministers and government officials by five litres per month, a 25% reduction in telephone expenses, and increasing the eligibility of MPs to receive a pension from five to 10 years. The magnitude of these cuts in government expenditure remains insignificant in contrast to the real need of the hour; especially when the Budget has made provisions to further expand the public sector, by offering permanent appointments to over 53,000 graduates which would drain a further Rs. 27,600 million from the exchequer. Such is counterintuitive to policies aimed at countering recurrent expenditure, and maintaining a bloated public sector is simply unaffordable with the current state of our public finances. Bold cuts to government expenditure would have reassured Sri Lanka’s creditors, donors, and lenders that we are serious about reforms while also making more resources and talent available to the private sector. Maintaining inflated departments with little or no productive output is a luxury we cannot afford anymore.

The continuation of financing this budget deficit through the domestic market borrowings will have a crowding out effect, especially as it will stunt credit available for the private sector and in return slow the country’s medium to long-term growth potential. Therefore, an ideal budget or a non-traditional budget would have prioritised fiscal consolidation. This includes setting a clear path to reduce the fiscal deficit to 5% by 2024. More efficient tax policy alternatives would have been reintroducing PAYE and withholding taxes and widening the tax base and spreading the tax burden to include a significant number of organisations that were given long tax breaks.

The Budget Speech highlighted three policies that, if implemented right, could direct the economy towards growth. The first being the acknowledgement that price controls have failed, and that market intervention creates uncertainties that affect consumers. This must be looked at with pragmatism, as the complete elimination of price controls including in the energy sector, can achieve better outcomes for the economy. The second being a policy focus to ensure a fair and competitive market. Recognising the role of the market economy and competition is a move in the right direction. This remains the only tried and tested solution to lower prices in the economy. The third policy that should be highlighted is the Finance Minister’s acknowledgement of a re-examination of the Samurdhi scheme. The scheme currently excludes some of the most vulnerable households and therefore, there is a need for tighter administration to ensure benefits accrue to those who need it most. The focus to streamline this initiative towards building entrepreneurship, fostering SMEs, and skill development is the right decision. However, for this to materialise, the Government needs to implement comprehensive reforms to improve ease of doing business and a comprehensive programme of digitalisation.

Addressing macroeconomic imbalances should have been a policy priority of the Budget. This includes addressing the fiscal deficit and the external current account deficit which have effects on the rest of the economy through interest rates and exchange rates. The Budget tries to address this issue by focusing on empowering local production. Prioritising self-sufficiency without opening the domestic market for competition is untenable. The Finance Minister’s speech outlined proposals to boost productivity, which are indeed pragmatic. Yet, one cannot increase productivity without improving competition. Focusing on improving national output has no economic impact without boosting domestic competition.

In the background, there was hope that the Government would start stabilising public finances, which would restore confidence. However, analysing the policy priorities of the Budget makes it clear that there has been little attempt to address the deficit and debt sustainability. Therefore, markets are unlikely to respond positively. At this juncture, Sri Lanka cannot afford to be complacent about our credit ratings. The Budget provided an ideal opportunity to provide a credible plan of action to get our credit ratings up. However, we seem to have missed this opportunity.

Measures to control public finances: spending, budget deficits, and debt

Year after year, the budget proposals have highlighted large-scale policies that remain limited to budget speeches. However, the present economic storm makes no space for such complacency. Hard structural reforms will need to be implemented inevitably. The Budget could have been the starting point. However, it seems that this window has passed. Therefore, there is a conscious need to build consensus for the implementation of key structural reforms that achieve macroeconomic stabilisation and long-term economic growth. Without macroeconomic stability, there will be no growth. Furthermore, these reforms need to be institutionalised. One way of doing this is the adoption of a medium-term fiscal and monetary framework that gives confidence to donors, lenders, investors, and citizens. Having such a framework will act as a clear sign that the State is committed to fiscal prudence and monetary stability. A medium-term expenditure framework is a tool for establishing public expenditure programmes within a coherent multi-year economic and fiscal framework.

Other key structural reforms for macroeconomic stabilisation, as outlined in Advocata’s Framework for Economic Recovery, include public finance management and public sector reforms, state-owned enterprise reforms, enhancing monetary policy effectiveness and maintaining exchange rate flexibility, supporting trade and investment to strengthen external trade, land reform, improving ease of doing business, and bridging infrastructure gaps. The only salvation to Sri Lanka’s present economic crisis is such a comprehensive reform package that goes beyond a traditional budget.

References:

MOF annual report 2020

CBSL Recent Economic Developments: Highlights of 2021 and prospects for 2022

https://www.treasury.gov.lk/api/file/0c3639d9-cb0a-4f9d-b4f9-5571c2d16a8b

https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=LK

K.D.D.B. Vimanga is a Policy Analyst at the Advocata Institute. He can be contacted at kdvimanga@advocata.org.

The Advocata Institute is an Independent Public Policy Think Tank. Learn more about Advocata’s work at www.advocata.org. The opinions expressed are the author’s own views. They may not necessarily reflect the views of the Advocata Institute